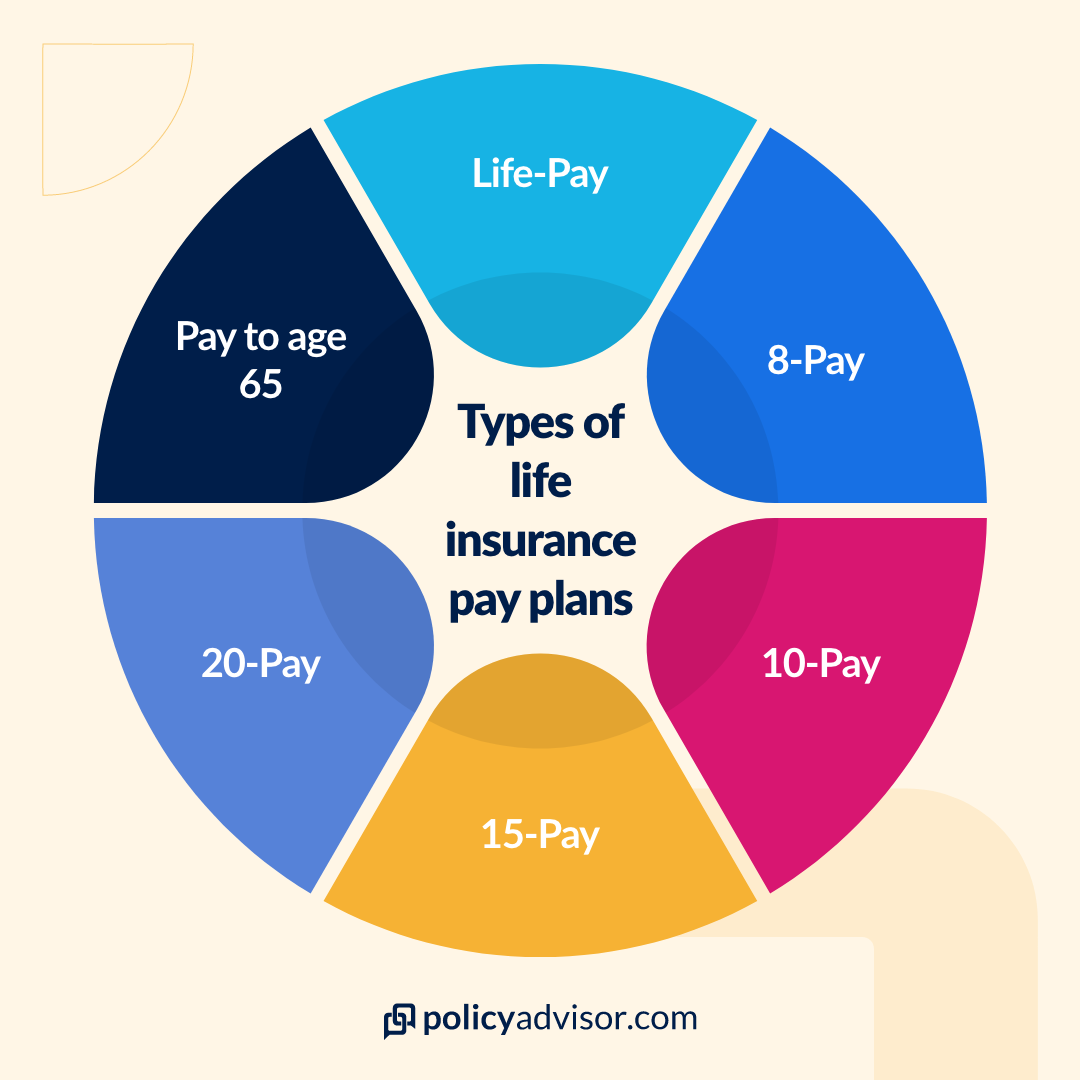

Some permanent life insurance policies allow you to pay your life insurance premiums on a condensed payment plan. These limited pay life insurance policies allow you to pay your premiums for a set amount of time (usually 10, 15, 20, or up to age 65), but you get continued coverage for the rest of your life. Some prefer limited pay plans as they only have to pay premiums in their best earning years and won’t have to worry about making payments while on a fixed retirement income.

By Carly Griffin Senior Insurance Advisor, LLQP 10 min read July 21st, 2023 IN THIS ARTICLEWhen completing a permanent life insurance policy application, there are several payment structures available. While many opt for monthly or yearly premium payments for the duration of their policy, it is also possible to choose quarterly, annual, or limited payment options. So, which one is the best deal and will give you the most bang for your buck? We’ll explore these options in further detail, with a special focus on limited pay life insurance options.

The cost of life insurance varies from person to person. Policy type and benefit amount play a big role in determining the cost of life insurance premiums, as do the age, health, smoking status, and occupation of the insured. For instance, a term life insurance policy has lower premiums than a whole life insurance policy; a 30-year-old non-smoker will have significantly lower premiums than a 30-year smoker, and a person with a history of medical conditions may have higher premiums than someone deemed healthy.

All that to say, the cost of life insurance is highly subjective to your individual circumstance and how the insurance company underwrites those circumstances . To navigate this topic in more depth head to our posts on the cost of life insurance and the cost of whole life insurance . You can also use our life insurance calculator to see how much you can expect to pay for the policy of your choice.

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

When purchasing a life insurance policy, there are a few payment structures to choose from. Term life insurance is straightforward: you either pay premiums every month or some insurance companies provide the option to pay premiums annually and offer a discount if you choose to do so.

PolicyAdvisor saves you time and money when comparing Canada’s top life insurance companies. Check it out!

Permanent life insurance, including whole life insurance policies and universal life insurance policies , have several more options for payment because of their lifelong coverage period.

Read more about the difference between whole life insurance vs. universal life insurance.

With a standard permanent life insurance policy, the policy owner is expected to make regular premium payments over the course of their lifetime. These payments keep the policy active and ensure continued coverage as well as a death benefit paid to the beneficiary . The standard payment structure for permanent life insurance has lower individual premiums payments than other options. Most policyholders choose to pay their premiums on a monthly or annual basis using this standard payment structure, but there is another option called limited pay .

A limited pay insurance policy is a type of permanent life insurance product, sometimes called whole life, in which the policyholder pays premiums over a set period of time or until a specific age. When the agreed-upon period ends, the policyholder stops paying life insurance premiums and coverage continues. In other words, a limited life insurance policy lets you pay your entire policy’s premiums over a set period of time rather than over a lifetime.

Because premiums are paid over a set period of time, individual premium payments tend to be quite high. For example, if your total premiums owed were $15,000 for a policy, spreading them out into 8 payments might be around $1875 each, whereas if you split the payments up over 20 years, you would only pay $750 each time.

Premium rates are therefore influenced by the chosen payment structure, size of the policy, as well as the insured’s age, health, smoking status, etc. It is important to note that an existing whole life insurance policy cannot be converted into a limited pay insurance policy.

With 8-pay whole life insurance, policyholders pay premiums for the first eight years of the policy. Because the initial policy value is accounted for in the first eight years (rather than accumulated over a lifetime of premium payments), there is greater potential for cash value growth and dividends. However, it’s important to keep in mind that because the lifetime payments are condensed, each payment will be high.

Permanent insurance policyholders have the option of customizing their own payment schedules. In other words, they can choose to pay premiums for the first 10 to 20 years of the policy. The length of the payment period is decided when the life insurance contract is signed.

This pay structure is similar to the others in that there is a point where you do not have to pay premiums anymore—but instead of a term, it cuts off at a specific age. These limited pay policies have age restrictions. For example, you wouldn’t be approved for a “to-age-65” policy if you are applying on your 64th birthday. In such a case, the policy would function more like a single-pay policy, which isn’t available on the Canadian market. This type of limited pay policy is beneficial to those who don’t want to pay insurance premiums in retirement age and want to keep premium costs lower than a 10, 15, or 20 pay structure.